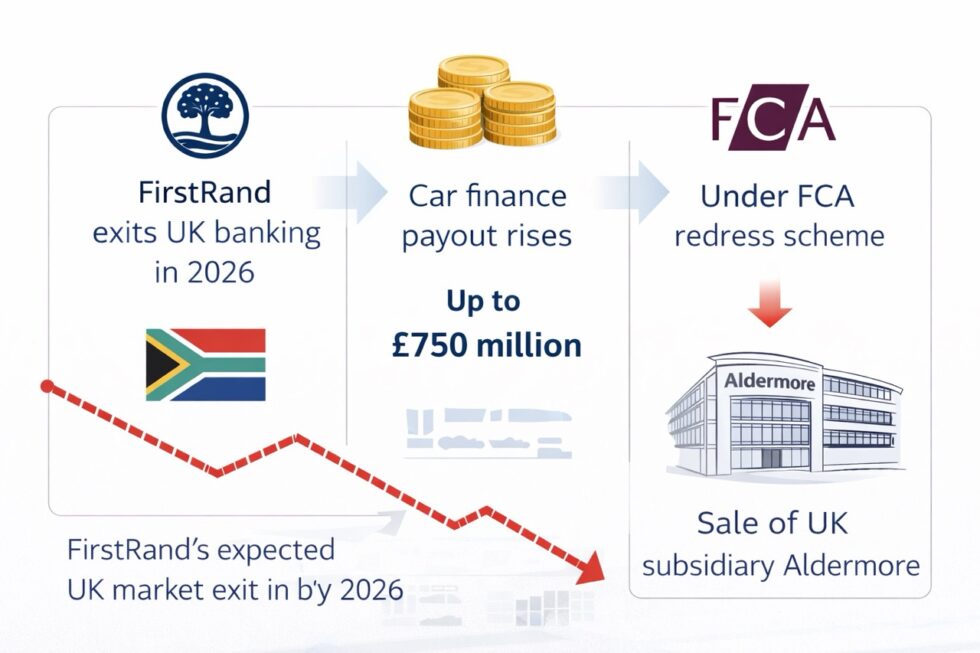

The decision by FirstRand to exit UK banking marks one of the most consequential breaks between an international lender and the UK regulatory system in recent years, after the South African banking group confirmed it would withdraw from Britain following a sharp escalation in its expected firstrand car finance payout, now estimated at up to £750 million and linked to the Financial Conduct Authority’s redress scheme — reported The WP Times, citing shareholder disclosures, regulatory statements and industry responses (FirstRand statement to shareholders, 8 April 2026; Financial Conduct Authority redress scheme publication, March–April 2026).

The announcement is not simply a corporate restructuring. It reflects a structural confrontation between regulatory intervention and the economic logic of banking operations, where retrospective compensation costs have begun to outweigh long-term profitability. In practical terms, FirstRand will work with the board of Aldermore — its UK subsidiary and the parent of MotoNovo — to facilitate what it describes as an “orderly ownership transition”, effectively putting a major UK lender up for sale as part of its exit strategy.

At the core of the dispute is the UK’s attempt to resolve the long-running car finance mis-selling scandal through a centralised redress scheme. The Financial Conduct Authority estimates the total cost to the industry could reach at least £9.1 billion. FirstRand, however, argues that the scheme’s design is fundamentally flawed, both in its methodology and in its scope, raising concerns that compensation may extend beyond customers who experienced demonstrable financial loss. Financially, the numbers are stark. The bank has increased its provision for compensation from £510 million to as much as £750 million — a figure that significantly exceeds the roughly £275 million in cumulative profit generated by its motor finance division over the previous decade (FirstRand financial update, 2026). This imbalance lies at the heart of the decision: a business line that was historically profitable is now expected to deliver a net loss on a scale that undermines its strategic viability.

How firstrand exits uk banking exposes tensions with regulators

The conflict between FirstRand and the FCA reflects a broader tension that has been building within the UK financial system: how to balance consumer protection with market stability. The FCA has positioned the redress scheme as the most efficient way to resolve a complex and fragmented set of complaints. According to the regulator, handling cases individually would cost firms more than £6 billion extra, prolong uncertainty and increase legal friction across the sector.

From the regulator’s perspective, the scheme is designed to create clarity and finality. By standardising compensation, the FCA aims to reduce the volume of litigation, limit operational burdens and restore trust among consumers who may have been affected by opaque commission structures in car finance agreements. However, FirstRand’s response highlights the risks inherent in such an approach. The bank has described the scheme as “deeply flawed in its construction”, suggesting that it may fail to accurately distinguish between customers who suffered genuine financial harm and those who did not. This concern is echoed by parts of the industry.

Shanika Amarasekara warned that overly broad compensation could distort outcomes:

“Where consumers suffered loss, redress must be paid. But any redress scheme for a market of this size must accurately identify and compensate only those customers who genuinely suffered loss” (industry statement, April 2026). She added that if the scheme is drawn too widely, it risks benefiting claims management companies rather than consumers — a dynamic that has been observed in previous financial compensation scandals in the UK.

This divergence in perspectives illustrates a fundamental policy dilemma. While regulators prioritise fairness and systemic resolution, banks must evaluate decisions through the lens of capital allocation, shareholder returns and long-term risk exposure. When those frameworks diverge too sharply, as in this case, the result can be market exit rather than adaptation.

The financial reality behind firstrand car finance payout

The escalation of the firstrand car finance payout is central to understanding why the bank chose to exit rather than absorb the costs. Moving from £510 million to £750 million is not merely an accounting adjustment — it represents a reassessment of the scale and depth of liability embedded within the UK car finance market. To place this in context, the motor finance division associated with MotoNovo generated approximately £275 million in profit over the past decade. The revised compensation estimate therefore implies that more than ten years of earnings could be effectively erased by a single regulatory intervention. This asymmetry between historical profitability and future liability creates a structural break in the business model. It raises a critical question for banks operating in regulated markets: how predictable are the rules under which profits are generated? For FirstRand, the answer appears to be that the UK market no longer offers sufficient predictability. The decision to exit is therefore not only about the current scheme but about the perceived risk of similar interventions in the future.

The wider industry is facing comparable pressures. Lloyds Banking Group has set aside around £2 billion for potential compensation, while Santander has provisioned close to £500 million (company disclosures, 2026). These figures underline the systemic nature of the issue: the redress scheme is not targeting a single institution but reshaping the economics of the entire sector. MotoNovo’s position is particularly significant. With an estimated 10% share of the UK car finance market, it represents a major player whose future ownership could influence competitive dynamics across lending, pricing and distribution channels. Any sale of Aldermore would therefore have implications beyond FirstRand’s balance sheet.

What happens next for aldermore and the UK banking market

The planned “orderly ownership transition” of Aldermore introduces a new phase in the story: who, if anyone, will be willing to acquire a UK banking asset under these conditions? Potential buyers will need to assess not only the immediate financial exposure linked to the redress scheme but also the broader regulatory environment. This includes the possibility of further claims, evolving interpretations of liability and the role of the UK Supreme Court in clarifying legal boundaries around commission disclosure and customer treatment. The outcome of these legal and regulatory processes will be critical in determining how risk is priced into future transactions. If uncertainty remains high, it could suppress valuations, reduce buyer appetite and slow the pace of consolidation within the sector.

At a macro level, the exit of FirstRand raises questions about the UK’s attractiveness as a financial market. Britain has long positioned itself as a global hub for banking and financial services, combining regulatory credibility with market depth. However, cases like this highlight the potential for tension between regulatory ambition and investor confidence.

For international banks, the key issue is not whether regulation exists — that is expected — but whether it is predictable, proportionate and stable over time. When large retrospective liabilities emerge, they can alter the perceived risk-reward balance in ways that are difficult to hedge or model. The car finance redress scheme may therefore have consequences that extend beyond consumer compensation. It could influence how global banks allocate capital, how they assess jurisdictional risk and how they structure their international operations.

The broader significance

The fact that firstrand exits uk banking is not an isolated corporate decision but a signal of a deeper structural shift. It reflects the growing complexity of operating in a regulatory environment where historical practices can be re-evaluated and monetised at scale years later.

For consumers, the scheme represents an attempt to correct past imbalances and ensure fairness. For banks, it introduces a new layer of uncertainty that must be priced into every business line. Between these two perspectives lies the future of the UK financial system — a balance that will determine not only how past issues are resolved, but how future investment decisions are made.

Read about the life of Westminster and Pimlico district, London and the world. 24/7 news with fresh and useful updates on culture, business, technology and city life: Fuel prices surge: what is the jet fuel price impact airlines and what happens next for travellers

Prepared using materials from:

Financial Conduct Authority statements, Reuters, FirstRand investor disclosures, UK financial sector reports, and coverage by BBC, The Telegraph and industry sources.