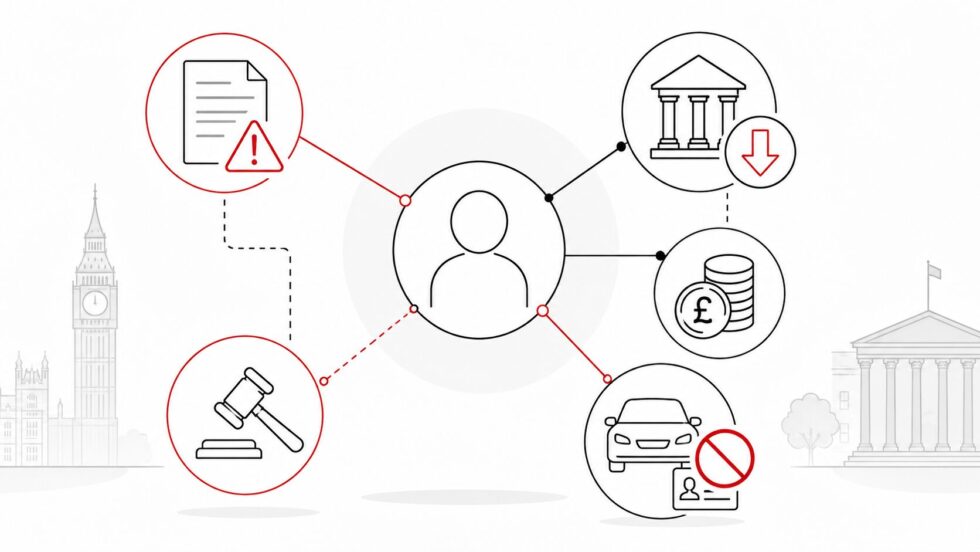

On 24 June 2026, the Department for Work and Pensions began sending updated warning letters to thousands of people across England, Scotland and Wales who still owe benefit debts after leaving the welfare system. The letters tell former claimants to contact the DWP, repay what they owe, challenge the debt if it is wrong or agree an affordable repayment plan before stronger enforcement begins from October 2026. Under the Public Authorities (Fraud, Error and Recovery) Act 2025, the department can now use tougher recovery powers, including direct deductions from bank accounts and court-backed driving licence orders in serious cases where a person can pay but refuses to engage, The WP Times reports.

The new DWP benefit debt powers do not mean every person with an overpayment will automatically lose their driving licence or have money removed from their account overnight. A driving sanction must go through the court, the debt must be at least £1,000, and the first order is normally suspended, meaning the person can keep driving if they follow the repayment terms set by the court. Direct bank deductions also come with a formal process: the DWP must assess affordability, review bank information and give the debtor time to make representations before money is recovered. The government says the crackdown is aimed at people who deliberately dodge repayment, while charities warn that vulnerable people, carers and those in financial hardship could be wrongly treated as refusing to engage if they do not understand or respond to official letters.

What changed on 24 June 2026 under the new DWP benefit debt rules

On 24 June 2026, the new welfare debt recovery powers came into force and the DWP began writing to people with outstanding benefit debts. The letters are not simply reminders. They are formal warnings that the department now has stronger legal routes to recover money from people who are no longer receiving benefits and are not repaying through standard deductions.

The policy mainly affects former claimants who owe money to the DWP but are outside the normal benefit payment system. In many cases, when someone is still receiving Universal Credit or another benefit, repayments can be taken from ongoing payments. The problem for the DWP has been people who have stopped claiming benefits, are not in PAYE employment, and are not voluntarily repaying what they owe. The new powers are designed to close that gap. From October 2026, enforcement will be rolled out gradually, giving affected debtors a four-month window from the first letters to contact the department, dispute the debt, pay it, or agree a repayment plan.

| Key point | What it means |

|---|---|

| Date letters began | 24 June 2026 |

| Enforcement rollout | From October 2026 |

| Main target group | People no longer receiving benefits who still owe DWP money |

| Bank account power | Direct Deduction Orders after safeguards and affordability checks |

| Driving licence power | Court-backed order only in serious cases |

| Debt threshold for driving sanction | At least £1,000 |

| Important protection | No disqualification where there is an essential need to drive |

Can DWP really ban someone from driving over benefit debt

The DWP cannot simply remove a driving licence by sending a letter. The department must apply to the court, and the court must decide whether a driving order is justified. This is an important detail because many headlines make the power sound automatic.

The first stage is usually a suspended disqualification order. That means the person is not immediately banned from driving. Instead, the court sets repayment terms. If the person keeps to those terms, they can continue driving. The risk of an actual driving ban arises if the person then fails to make more than one ordered payment, or fails to make the final payment, without a reasonable excuse. An immediate driving disqualification can last up to two years, but it must end once the debt is fully repaid. The order is handled through the legal process and DVLA records, not by DWP physically taking a licence card at the door. The most important safeguard is essential need. A court should not disqualify someone if they need their licence for work, caring responsibilities, disability-related travel, medical appointments or other essential daily responsibilities.

How could DWP take money directly from bank accounts

The new Direct Deduction Order power allows the DWP to recover money from a bank or financial institution without first getting a court order. But it is not meant to be an instant seizure without checks. Before making a Direct Deduction Order, the DWP should assess affordability and examine financial information, including recent bank statements. The purpose is to understand whether the person has enough money to repay, whether deductions would cause hardship, and what level of repayment could be reasonable.

The debtor must be notified and given time to respond. If the account is joint, the other account holder should also be informed. The person can make representations, explain hardship, challenge the amount, or ask for a different repayment arrangement. If they disagree with the final decision, there should be a route to review or appeal. For readers, the practical point is clear: if a DWP bank deduction notice arrives, the person should not wait. They should respond before the deadline, provide evidence of essential costs and ask for an affordable repayment plan if the debt is correct.

Who is most likely to receive a DWP benefit debt letter

The letters are most likely to go to people who have an outstanding debt to the DWP and are no longer receiving the benefit from which repayments could normally be deducted. This could include former Universal Credit claimants, people with historic benefit overpayments, people who had changes in earnings or household circumstances, or those who received money they were not entitled to.

Not every debt is fraud. Some debts arise because earnings were not reported correctly, but others come from late updates, misunderstanding benefit rules, relationship changes, housing cost errors, Carer’s Allowance issues, disability benefit decisions or mistakes made by the department itself. That is why the first step is to check the debt, not panic. A person should ask what benefit the debt relates to, what period it covers, how the amount was calculated and whether the DWP believes the issue was fraud, claimant error or official error.

What should people do now if they get a DWP letter

Anyone who receives a DWP debt letter should treat it as urgent, especially because stronger enforcement begins from October 2026. The safest response is to contact the department early, even if the person disputes the debt. The first action is to ask for a full breakdown. The second is to check whether the amount is correct. The third is to explain financial circumstances and ask for an affordable repayment plan if the debt is accepted. The fourth is to tell the DWP immediately if driving is essential for work, care, disability, health or family responsibilities.

Useful evidence can include payslips, rent statements, childcare costs, energy bills, medical letters, caring documents, employer letters, self-employment records, delivery driver records, bank statements and proof of transport needs. The worst mistake is silence. If a person ignores letters because they are anxious, unwell or overwhelmed, the case may look like deliberate non-engagement. That is why debt charities are warning that vulnerable people need support before enforcement begins.

From 24 June 2026, DWP has started warning people with unpaid benefit debts that stronger recovery powers are now available. From October 2026, the department can begin using those powers more actively, including direct bank deductions and court-backed driving licence orders in serious cases. But the detail matters. A driving ban is not automatic, the debt must be at least £1,000, the court must be involved, and essential need to drive must be considered. Bank deductions also require process, notice and affordability checks. Anyone who receives a letter should respond early, check the debt, challenge mistakes, explain hardship and agree only to a repayment plan they can realistically afford.

FAQ: DWP benefit debts, bank deductions and driving bans

Can DWP ban people from driving over benefit debts?

Yes, but not automatically. DWP cannot simply take away a driving licence by sending a letter. In serious cases, DWP must apply to a court for a driving disqualification order. The debt must normally be at least £1,000, and the court must consider whether the person has an essential need to drive.

When did the new DWP powers start?

The new powers came into force on 24 June 2026. From that date, DWP began sending updated warning letters to people with unpaid benefit debts. Stronger enforcement is expected to be rolled out gradually from October 2026.

Can DWP take money directly from bank accounts?

Yes. Under the new rules, DWP can use Direct Deduction Orders to recover unpaid benefit debts from bank accounts. However, this should involve safeguards, including affordability checks, notice to the debtor and time to respond before deductions begin.

Who is most at risk under the new DWP debt rules?

The rules mainly affect people who no longer receive benefits but still owe money to DWP. This could include former Universal Credit claimants or people with old benefit overpayments who are not repaying the debt through benefits or PAYE deductions.

Does every benefit debt lead to a driving ban?

No. A driving ban is meant for serious cases where someone is judged to be refusing to repay despite being able to do so. The court process, the £1,000 debt threshold and essential-need protections make it a last-resort measure, not a standard penalty.

What counts as an essential need to drive?

An essential need may include driving for work, caring responsibilities, disability-related travel, medical appointments or living somewhere where public transport is not a realistic option. People should provide evidence such as employer letters, medical documents or caring records.

What should people do if they receive a DWP debt letter?

They should not ignore it. The safest steps are to check the amount, ask for a full breakdown, challenge the debt if it looks wrong, explain financial hardship and ask for an affordable repayment plan before enforcement begins.

Can vulnerable people be affected?

Yes, and this is one of the main concerns raised by debt advisers and charities. Some people may fail to reply because of illness, mental health problems, caring responsibilities, disability, language barriers or financial stress. That can look like non-engagement, so it is important to ask for support early.

What if the DWP debt is wrong?

The person should challenge it as soon as possible and ask DWP to explain the benefit, period, calculation and reason for the overpayment. If the debt involves Universal Credit, PIP, Carer’s Allowance or housing costs, specialist welfare advice may be useful.

What is the key date for enforcement?

The key warning date is 24 June 2026, when letters began. The key enforcement date is October 2026, when stronger recovery powers are expected to start being used gradually.

Read about the life of Westminster and Pimlico district, London and the world. 24/7 news with fresh and useful updates on culture, business, technology and city life: Shrek 5 official teaser trailer reveals the ogre’s 2027 return — and a fan debate over the new look